Wind Energy Reports

Industry electrification in a renewable power system

This paper is about the gradual electrification of industry and its relation to the growing penetration of variable renewable electricity generation. The interaction between these developments can significantly reduce the challenges associated with either of them.

Decarbonizing the energy system is very challenging. However, it is essential to limit global warming to acceptable levels. The main pathway to decarbonization – replacing fossil fuels with renewable energy – is not straightforward. For the energy system, it involves installing large amounts of variable renewable electricity generation. However, a large installed capacity of renewable electricity sources leads to increasingly longer periods where generation exceeds demand (‘surplus’ electricity), while on the other hand, periods where renewable electricity generation is insufficient to meet demand remain. Because of the simultaneity of variable renewable generation, an increase of its installed capacity leads eventually to an increasing need to curtail during oversupply and thus to a reduced yield of added variable renewable capacity. This will threaten the business case for new variable renewables. The increase in renewable electricity generation capacity and the potential mismatch with electricity demand leads to issues for the market as well as for the infrastructure:

1 Market issues

An electricity price of zero for electricity when there is a surplus1 and high electricity prices during shortage.

2 Infrastructure issues

Constraints in the electricity grid that limit the transportation and distribution capacity.

Storage and demand response – such as shifting electricity demand to match variable generation – are seen as solutions. Especially lithium-ion batteries are very well-equipped to accommodate load swings of up to one day. The effect of storage and demand shift on electricity prices is twofold: it creates demand at very low electricity prices, and it increases electricity supply at high prices, mainly caused by a (relative) shortage of variable renewable generation. This leads to a significant reduction in the need to curtail variable renewable electricity in terms of MWh, but unfortunately not as much in terms of the duration of curtailment. This means that, with an increasing amount of storage, the price-boosting effect of storage during charging will increasingly be offset by the price-reduction effect of discharging. Hence, a large capacity of storage and demand shift will have a limited impact on the overall business case for variable renewables. Demand response that does not rely on shifting demand is another option that is especially suited to free up capacity in emergency situations. This may for instance involve shutdown of operations or industrial demand response capable of falling back on other energy carriers, such as biomass, natural gas, and eventually hydrogen. Such demand response is characterized by ‘opportunity costs’, i.e. the cost of curtailing production (generally expensive) or the cost of switching to the alternative energy carrier (generally relatively cheap). In this report, we call the latter ‘opportunity demand’.

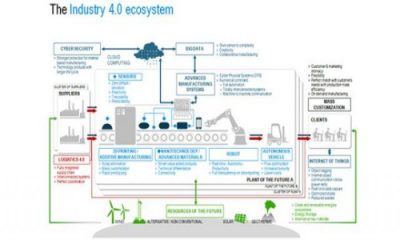

Gradual decarbonization of industry For industry, the primary path towards decarbonization is electrification, preferably using renewable sources. In this report, we looked at using opportunity demand for industrial heating, i.e. heat supply that is capable of switching between gas boilers and electric boilers depending on the price difference between natural gas and electricity. Taking Germany as an example, our case-study calculations show that a structurally positive commercial business case is emerging for a hybrid electric-gas system for large-scale industrial heating, provided that the industry is exposed to ETS carbon prices and that synergies with the grid allow for low grid tariffs similar to industry with large continuous electricity load. Hence, opportunity demand can be an economically attractive way to decarbonize industrial heating.

Setting a price for renewable electricity Opportunity demand increases demand during renewable surplus, but not during shortage. Because it is triggered by opportunity cost (the fuel price, e.g. for gas or biomass) and not directly related to the current or future electricity price, it can set a price for electricity. In an energy system with plenty of renewables and with sufficient opportunity demand and storage, the price-setting effect is amplified by storage, because storage will take the opportunity cost based on (predominately) natural gas as the low-price reference for charging, instead of an electricity price of zero set by surplus renewables. From a societal point of view, renewable generation should preferably be stimulated indirectly. By stimulating the demand for variable renewable electricity rather than generation directly, a better fit is ensured between supply and demand, ultimately reducing curtailment of renewable generation. The main bottleneck for the electrification of industry through opportunity demand appears to be the increased need for transmission capacity in the electricity network. This is reflected in a significant increase of the grid fee covering transmission costs for the electric boiler (or electrolyser).

Infrastructure constraints

The German business case for opportunity heating highlights the need for an integrated view on the energy transition that should optimally utilize the synergies between the various aspects of the energy system. There are still significant synergies possible between variable renewable generation, flexible demand with a theoretically infinite sustain time, and the electricity network. We briefly discuss three of them: non-firm capacity, interruptible capacity, and capacity pooling. Compared to congestion management, the latter two options offer the additional advantage of opportunity demand, potentially giving industry a more secure and sustained coverage for the required investments. In this paper, we define non-firm capacity as capacity for generation or demand that can be shed in advance to avoid congestion. We define interruptible capacity as capacity that can be instantaneously shed to free up capacity for higher-priority load. Because of this, it can make use of the reserve capacity in the transmission system needed to preserve the N-1 redundancy criterion. An alternative way of looking at it is that the load provides an ‘N-1 service’ to the network. With capacity pooling, several loads and generation units in a confined geographical area collectively contract capacity and are free to share it between themselves, as long as their total used capacity remains within the boundaries agreed upon with the grid operator. This allows the participants to exploit the synergies between their loads. We show that significant synergies can be achieved through smart electrification of industry by applying opportunity demand to reduce the impact on the network and even help to reduce the impact of variable renewable electricity generation.

Conclusions

In summary:

Opportunity demand, especially for industrial heating, is becoming an economically attractive way for industry to gradually electrify using renewable electricity and can become an important mechanism to support the energy transition.

Opportunity demand supports the business case for renewables and for electricity storage. It provides a floor price for electricity based on the cost of the alternative (e.g. natural gas instead of electricity for industrial heating), thus avoiding zero prices.

Opportunity demand is well-suited to optimize the use of the electricity transportation and distribution grid. It can be applied as non-firm capacity, as interruptible capacity, or for capacity pooling. All three mechanisms promote optimal use of the grid.

Wind Energy Reports

Offshore wind installed capacity reaches 83 GW as new report finds 2024 a record year for

The Global Wind Energy Council’s flagship Global Offshore Wind Report, released today, shows that the offshore wind industry added another 8GW of capacity in 2024, making it the fourth highest year ever. This brings total installed offshore wind capacity globally to 83 GW – enough to power 73 million households.

Government auctions awarded 56 GW of new capacity globally last year, a record figure, while the industry is already constructing another 48 GW of offshore wind worldwide, also a record figure. The report highlights the significant policy and regulatory breakthroughs that are forming the next stage of offshore wind markets in countries including Japan, South Korea and the Philippines.

However, despite the strong pipeline, the report shows that macroeconomic headwinds, failed auctions, supply chain constraints and increasing policy instability, particularly in the US, have contributed to a downgrading of GWEC’s short term outlook.

The report warns that, whilst the fundamental case for offshore wind has never been stronger, the sector is facing an inflection point. GWEC recommends that industry and governments now need to urgently work together to redesign auction processes to focus on delivery and better risk sharing so that offshore wind can fulfil its vital role in providing large scale and secure clean power. The report also finds that the fundamentals of offshore wind have not changed, and the mid-term outlook remains strong.

GWEC’s Global Offshore Wind Report shows there is now 83GW of offshore wind capacity across the world, enough to power 73 million households. GWEC’s Market Intelligence team forecasts annual offshore wind capacity installations to grow from 8GW in 2024 to 34GW in 2030. However, GWEC’s short-term outlook is 24% lower than the previous year’s forecast due to a negative policy environment in the US and auction failures in the UK and Denmark. Adding to these challenges are transmission delays in Europe and slower commissioning in the APAC region, meaning that, while growth continues, it is happening at a slower pace.

Annual growth rates are expected to be 28% until 2029, and 15% up to 2034, which, in capacity-terms, means the industry will still sail past the milestones of 30GW annually in 2030 and 50 GW by 2033.

While near-term growth is concentrated in the already established markets in Europe and China, GWEC reports offshore wind pushing into new regions such as Asia-Pacific and Latin America. In Japan, South Korea, Philippines, Vietnam, Australia, Brazil and Colombia, government is working with the industry to establish policies and regulations to fast-track offshore wind. This signals policymaker commitment and sets the stage for the sector’s next wave of market expansion.

The Key Data

In 2024, 8 GW of new offshore wind capacity was grid-connected worldwide. New additions were 26% lower than the previous year, making 2024 the fourth-highest year in offshore wind history.

The global offshore market grew on average by 10% each year in the past decade, bringing total installations to 83.2 GW, which accounted for 7.3% of total global wind capacity as of the end of 2024.

China led the world in new offshore wind installations for the seventh year in a row, followed by United Kingdom, Taiwan (China), Germany and France. The top five markets made up 94% of the new additions in 2024.

China is the absolute market leader for cumulative offshore wind installations, accounting for half of the global market share, followed by the UK. Germany, the Netherlands and Taiwan (China) complete the top five. Offshore wind pioneer Denmark dropped out of the top five for the first time.

At the end of 2024, a total of 278 MW net floating wind was installed globally, of which 101 MW in Norway, 78 MW is in the UK, 40MW in China, 27MW in France, 25 MW in Portugal, 5 MW in Japan and 2 MW in Spain.

The report forecasts a compound average growth rate of 21% for the offshore wind industry, which means another 350 GW of offshore wind energy capacity to be added over the next decade (2025–2034), bringing total offshore wind capacity to 441 GW by the end of 2034.

Annual offshore wind installations are expected to double in 2025, triple in 2027 and then sail past the milestones of 30 GW in 2030. By 2034, they are expected to reach 55 GW, bringing the offshore share of new wind power installations from today’s 7% to about 25%.

China and Europe will continue to dominate offshore wind growth going forward but their global market share in cumulative installations is expected to drop to 89% in 2029 and 84% in 2034, because of growth in markets outside the two key markets in APAC, North America and Latin America.

More than 500,000 new wind technicians needed by 2028 if industry it to meet global wind energy ambitions, new report from GWEC and GWO finds.

The world will need 532,000 new wind technicians by 2028 to meet the increasing demand for onshore and offshore wind, according to the Global Wind Workforce Outlook, a new report from the Global Wind Energy Council and Global Wind Organisation. The report finds that 40% of those roles will need to be filled by new entrants, highlighting the need for a resilient supply chain of skilled personnel to build and maintain wind fleets.

To meet global wind power ambitions and ensure wind energy plays the role required for net zero and global renewables targets, it is vital governments and industry work to grow the workforce.

The next era of wind energy needs government to invest in vocational training and support international training standards. These steps play an important role supporting a just and equitable energy transition away from fossil fuels, while offering win-wins that advance socioeconomic opportunities, ensure safety and supporting stable growth within the wind industry.

The report details nine steps policymakers can take to address help fulfil the mid-tolong- term workforce needs:

1. Set workforce targets as part of the national energy policy to support wind or renewable energy installation targets.

2. Introduce education courses based on science, technology, engineering and mathematics (STEM) for preparing students to become the entry level wind workforce.

3. Investments and funding programs for workforce training, apprenticeships and upskilling to equip workers with the skills needed for wind and renewable energy jobs, especially offshore wind.

4. Promote industrial policy and tendering criteria that foster wind installation growth through local jobs as much as possible.

5. Facilitate the tailored retraining/ reskilling pathways to promote transfer and upskilling of workers from carbon intensive industries to wind industry jobs.

6. Promote diversity, equity and inclusion to resolve skill shortages by enhancing attraction and retention of workers to the industry.

7. Make strategic policy improvement to address workforce imports, exports and dislocation.

8. Set standards and penalty provisions for operational health and safety for onshore wind and offshore wind workforce.

9. Embrace the advantages of global standards and workforce initiatives, blending them to meet local conditions.

Ben Backwell, CEO of the Global Wind Energy Council, said: “As the global wind energy sector continues to grow, particularly in new markets, it is crucial that the growing wind workforce is equipped with the right training and tools to meet the increasing demand. Deployment must be accelerated to meet net zero and global renewable targets, meaning it is vital that government and industry work together to build a workforce capable of delivering onshore and offshore wind.

“The nine steps outlined in this report provide a roadmap for action that can help turn ambitions into projects on the ground. GWEC is working with global, regional and national stakeholders to ensure wind energy fulfils its role in the energy transition. Building a strong workforce capable of supporting a scaledup industry is key to that potential being fulfilled.”

Jakob Lau Holst CEO, Global Wind Organisation, said: “The message from this, our fifth edition of the GWWO, is clear: a focus on people is essential to meet wind sector goals and drive a sustainable energy transition. GWO & GWEC’s programmes and partnerships have a key role in acting to reduce the impact of climate change on communities. However, to achieve resilient supply chains of skilled personnel ready to build and maintain the wind energy infrastructure we also need governments to act by investing in vocational training, removing regulatory barriers and by supporting the call for international training standards.

“The Global Wind Workforce Outlook focuses on areas critical to the final stages of wind energy commissioning, the key stage that turns projects in planning into projects in operation. Addressing workforce shortages here can rapidly accelerate growth and play a key role in ensuring wind plays its role in combating climate change.

Brian Allen, CEO, Beam, said: “The Global Wind Workforce Outlook illuminates both the scale of our industry’s workforce challenge and the transformative opportunities ahead. We know that technology and innovation are key enablers to unlocking the full potential of wind power, as rapid scaling will be essential to meet future energy demands. But, as the Outlook shows, deployment of offshore wind depends not only on technological advancement but on our ability to build, nurture, and retain a skilled workforce. The convergence of AI innovation and workforce transformation will be vital for accelerating the global transition to renewable energy.”

The report examines ten countries in detail; Australia, Brazil, China, Germany, India, Philippines, Republic of Korea, Saudi Arabia, South Africa and the United States of America. Training needs in these 10 countries constitute 73% of the total number of C&I and O&M technicians forecast to be working in the sector in 2028.

The global Wind Power Market size was valued at USD 95.16 billion in 2023 and is projected to grow from USD 106.42 billion in 2024 to USD 254.27 billion by 2031, exhibiting a CAGR of 13.25% during the forecast period. Growing adoption of offshore wind farms and surge in wind energy projects are augmenting market growth.

The growing adoption of offshore wind farms is a significant trend in the wind power market. Offshore wind farms are being increasingly developed due to their numerous advantages over onshore counterparts. They benefit from stronger and more consistent wind speeds prevalent over the ocean, leading to higher energy yields and improved efficiency.

Additionally, offshore wind farms reduce land use conflicts, as they are situated away from populated and agricultural areas. Government incentives and advancements in technology are key factors fueling this trend. Many countries are offering subsidies, tax incentives, and supportive policies to promote the development of offshore wind projects.

Technological advancements, such as the development of larger and more efficient turbines designed to withstand harsh marine environments, are making offshore wind farms more viable and cost-effective. This trend contributes to lowering carbon emissions and reducing reliance on fossil fuels, thereby playing a crucial role in meeting the increasing global demand for renewable energy sources.

Wind Power Market Trends

The integration of wind power with energy storage systems is an emerging trend that addresses its intermittency, which represents a significant limitation of wind energy. By pairing wind turbines with advanced storage solutions, such as lithium-ion batteries or pumped hydro storage, the energy generated during peak wind periods is stored and used during times of low wind activity or high demand. This trend is gaining significant traction due to advancements in energy storage technologies, which are enhancing efficiency and cost-effectiveness. The combination of wind power and storage systems enhances the reliability and stability of the electricity supply, making wind energy a more viable and consistent source of renewable energy.

Additionally, integrated storage systems help mitigates the impact of sudden fluctuations in wind power generation on the grid, thereby reducing the need for backup fossil fuel-based power plants. This trend is supported by government policies and incentives aimed at promoting the adoption of renewable energy and energy storage technologies.

Wind Power Market Regional Analysis

Based on region, the global market is classified into North America, Europe, Asia-Pacific, MEA, and Latin America. Asia-Pacific wind power market accounted for a significant share of 36.25% and was valued at USD 34.50 billion in 2023, reflecting the region’s significant commitment to renewable energy development. The rapid expansion of wind power in Asia-Pacific is reinforced by the growing energy needs of its populous nations, particularly China and India, which are making substantial investments in both onshore and offshore wind projects. China has emerged as major country in wind power capacity due to its aggressive renewable energy targets, extensive government support through subsidies, and favorable policies.

Moreover, India’s national wind-solar hybrid policy and other initiatives are bolstering wind energy deployment. The region’s abundant wind resources, coupled with technological advancements and decreasing costs of wind power generation, are propelling domestic market growth. Additionally, the increasing environmental awareness and the urgent need to reduce greenhouse gas emissions are prompting countries across Asia- Pacific to adopt wind energy as a key component of their energy strategies.

North America is set to grow at a robust CAGR of 13.35% in the forthcoming years, largely attributable to several factors such as ongoing technological advancements, supportive regulatory frameworks, and increasing investments in renewable energy. The incentives are prompting utilities and independent power producers to invest in new wind projects. Additionally, advancements in wind turbine technology, including the production of larger and more efficient turbines, are reducing the cost of wind energy, thereby enhancing its competitiveness compared to traditional energy sources.

For instance, in 2023, according to US Department of Energy, Wind energy in the United States contributed to the reduction of 336 million metric tons of carbon dioxide emissions annually, which is equivalent to the emissions generated by 73 million cars.

Canada is further supporting this growth with its favorable wind resources and supportive provincial policies aimed at expanding renewable energy capacity. The commitment to sustainability and reducing carbon emissions is leading to the widespread adoption of wind energy in North America.

Events8 years ago

Events8 years agoCanada and Turkey women working in the renewable energy sector in met

- Turbine Technologies7 years ago

GE’s Haliade-X 12 MW prototype to be installed in Rotterdam

- Operations and Maintenance8 years ago

GENBA is on the rise; another milestone passed by in global existence

- Genel11 years ago

EWT launches the DW61, It’s most efficient and high energy producing wind turbine

- Genel11 years ago

Internet of things will empower the wind energy power plants

- Turbine Technologies8 years ago

İğrek Makina focused on developing and producing Machine Tools and Wind Energy Turbines

- Legal & Financial Solutions7 years ago

Demand/Supply – Renewable energy with guarantees of origin (GO)

- Events7 years ago

Key Players from 10 Nations will Show Their Strong Positions at APWEE

- Turbine Technologies6 years ago

ENERCON installs E-160 EP5 prototype

- Turbine Technologies7 years ago

The Nordex Group receives first order for Delta4000 turbines from the USA

- Turbine Technologies8 years ago

ENERCON and Lagerwey together develop two new WEC types

- Genel10 years ago

Zorlu energy envisages a bold new future based on renewables